Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

The Truth About Down Payments

If you’re planning to buy your first home, saving up for all the costs involved can feel daunting, especially when it comes to the down payment. That might be because you’ve heard you need to save 20% of the home’s price to put down. Well, that isn’t necessarily the case.

Unless specified by your loan type or lender, it’s typically not required to put 20% down. That means you could be closer to your homebuying dream than you realize.

As The Mortgage Reports says:

“Although putting down 20% to avoid mortgage insurance is wise if affordable, it’s a myth that this is always necessary. In fact, most people opt for a much lower down payment.”

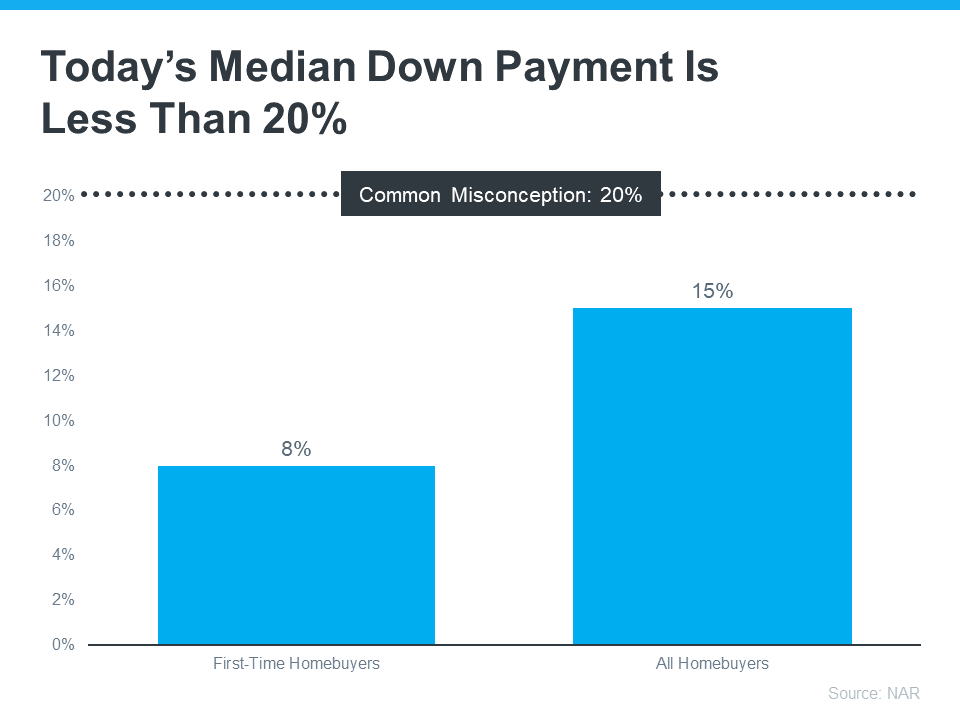

According to the National Association of Realtors (NAR), the median down payment hasn’t been over 20% since 2005. In fact, for all homebuyers today it’s only 15%. And it’s even lower for first-time homebuyers at just 8% (see graph below):

The big takeaway? You may not need to save as much as you originally thought.

Learn About Resources That Can Help You Toward Your Goal

According to Down Payment Resource, there are also over 2,000 homebuyer assistance programs in the U.S., and many of them are intended to help with down payments.

Plus, there are loan options that can help too. For example, FHA loans offer down payments as low as 3.5%, while VA and USDA loans have no down payment requirements for qualified applicants.

With so many resources available to help with your down payment, the best way to find what you qualify for is by consulting with your loan officer or broker. They know about local grants and loan programs that may help you out.

Don’t let the misconception that you have to have 20% saved up hold you back. If you’re ready to become a homeowner, lean on the professionals to find resources that can help you make your dreams a reality. If you put your plans on hold until you’ve saved up 20%, it may actually cost you in the long run. According to U.S. Bank:

“. . . there are plenty of reasons why it might not be possible. For some, waiting to save up 20% for a down payment may “cost” too much time. While you’re saving for your down payment and paying rent, the price of your future home may go up.”

Home prices are expected to keep appreciating over the next 5 years – meaning your future home will likely go up in price the longer you wait. If you’re able to use these resources to buy now, that future price growth will help you build equity, rather than cost you more.

Bottom Line

Keep in mind that you don’t always need a 20% down payment to buy a home. If you’re looking to make a move this year, let’s connect to start the conversation about your homebuying goals.

When You Sell Your House, Where Do You Plan To Go?

If you’re thinking about selling your house, you may have heard the supply of homes for sale is still low, and that means your house should stand out to buyers who are craving more options. But you may also be wondering, once you sell, how does the current supply impact your own move? And, will you be able to find a home you want to buy with inventory this low?

One thing that can help you find your next home is exploring all your options, including both homes that have been lived in before as well as newly built ones. Let’s look at the benefits of each one.

The Pros of Newly Built Homes

First, let’s look at the advantages of purchasing a newly constructed home. With a brand-new home, you’ll be able to:

- Create your perfect home. If you build a home from the ground up, you’ll have the option to select the custom features you want, including appliances, finishes, landscaping, layout, and more.

- Cash-in on energy efficiency. When building a home, you can choose energy-efficient options to help lower your utility costs and reduce your carbon footprint.

- Minimize the need for repairs. Many builders offer a warranty, so you’ll have peace of mind on unlikely repairs. Plus, you won’t have as many little projects to tackle.

- Have brand new everything. Another perk of a new home is that nothing in the house is used. It’s all brand new and uniquely yours from day one.

The Pros of Existing Homes

Now, let’s compare that to the perks that come with buying an existing home. With a pre-existing home, you can:

- Explore a wider variety of home styles and floorplans. With decades of homes to choose from, you’ll have a broader range of floorplans and designs available.

- Join an established neighborhood. Existing homes give you the option to get to know the neighborhood, community, or traffic patterns before you commit.

- Enjoy mature trees and landscaping. Established neighborhoods also have more developed landscaping and trees, which can give you additional privacy and curb appeal.

- Appreciate that lived-in charm. The character of older homes is hard to reproduce. If you value timeless craftsmanship or design elements, you may prefer an existing home.

The choice is yours. When you start your search for the perfect home, remember that you can go either route – you just need to decide which features and benefits are most important to you. As an article from The Mortgage Reports says:

“When building, you gain more freedom to tailor the design, materials, and features, but it demands more time and involvement. Conversely, buying an established home offers immediate occupancy . . . yet may require compromises. Your choice should align with your budget, timeline, customization preferences, and the local real estate landscape.”

Either way, working with a local real estate agent throughout the process is mission-critical to your success. They’ll help you explore all of your options based on what matters most to you in your next home. Together, you can find the home that’s right for you.

Bottom Line

If you have questions about the options in our area, let’s discuss what’s available and what’s right for you. That way you’ll be ready to make your next move with confidence.

Thinking About Using Your 401(k) To Buy a Home?

👻 The scariest night of the year is upon us so here’s a look at the most terrifying renovations to add value to your home this Halloween.

Spooky features to add value this Halloween

👻 The scariest night of the year is upon us so here’s a look at the most terrifying renovations to add value to your home this Halloween.

Prices Break $400k Barrier Again

💸 American property prices continue to defy the gravity of higher mortgage costs with values rising for a fifth consecutive month.

Your Home Equity Can Offset Affordability Challenges

📊 Mortgage rates may be making you wonder if selling is the right decision. Here’s what you need to know about how home equity can help.

Why Is Housing Inventory So Low?

🏡 Why is it so hard to find a house to buy? And while it may be tempting to wait it out until you have more options, that’s probably not the best strategy. Here’s why.

Get Ready for Smaller, More Affordable Homes.

🏡 In some ways, smaller homes are already here. When the pandemic hit, the meaning of home changed. People needed the space their home provided not only as a place to live, but as a place to work, go to school, exercise, and more.

Expert Home Price Forecasts Revised Up for 2023

📈 Toward the end of last year, there were a number of headlines saying home prices were going to fall substantially in 2023

Gen Z: The Next Generation Is Making Moves in the Housing Market

💁🏽♀️ Generation Z (Gen Z) is eager to put down their own roots and achieve financial independence. As a result, they’re turning to homeownership.